global@hmeonline.com

Mon to Fri 09:00 – 17:30

In recent years, with the acceleration of the global industrialization process and the rapid development of the new energy automobile industry, the consumption of power batteries has also increased. The current status of metal materials required for power batteries in China is "more titanium and manganese, less lithium, and lack of cobalt and nickel", and most of these materials rely on imports. In the long run, will this situation restrict the development of China's new energy industry and become another "stuck neck" factor? What is the current development status of China in the field of new energy materials? What are the opportunities for cooperation with ASEAN in the future? Recently, at the "2021 China-ASEAN Petroleum and Chemical International Cooperation Forum" held in Qinzhou, Guangxi, the participating experts conducted in-depth discussions on a series of topics related to this.

China has become the world's largest producer of lithium-ion batteries for 5 consecutive years

Xu Haidong, deputy chief engineer of the China Association of Automobile Manufacturers, pointed out that since 2015, China's new energy vehicle production, sales and ownership have ranked first in the world for five consecutive years, with a total of more than 6 million vehicles promoted, accounting for more than 50% of the world, and it has entered a new stage of accelerated development. . In 2020, the production and sales of new energy vehicles will be 1.366 million and 1.367 million, a year-on-year increase of 7.5% and 10.9% respectively.

Beginning in 2015, driven by China's vigorous development of new energy vehicles, the scale of China's lithium-ion battery industry began to grow rapidly. In 2015, it surpassed South Korea and Japan to rank first in the world, and gradually widened the gap.

Liu Yanlong, Secretary-General of the China Chemical and Physical Power Supply Association, said that the 2020 global lithium-ion battery industry is mainly concentrated in China, Japan, and South Korea. Although China's power battery has been affected by the dual impact of the new crown pneumonia epidemic and subsidy decline, the scale growth rate has slowed down. Still in a stage of rapid growth, lithium-ion batteries account for 53.8% of the world's total, making it the world's largest producer of lithium-ion batteries.

At present, the global power battery industry reshuffle is accelerating, the competitive landscape of leading companies is relatively stable, and other companies will gradually be marginalized. In 2020, CATL continued to rank first in the world with 34GWh of installed capacity. LG New Energy, driven by Tesla and the European market, achieved 31GWh of installed capacity, ranking second, followed by Panasonic, BYD, Samsung SDI and other companies. Among the top ten companies are five Chinese companies, two Japanese companies and three South Korean companies.

In 2020, China's new energy vehicles will have 72 supporting power lithium-ion battery companies, which is a decrease of 7 compared with 2019. Compared with the top 10 power battery installed capacity in 2019, BAK Battery and Xinwangda have fallen out of the top 10 list. Others Eight power battery companies remained stable in the top 10 ranks, with LG Chem and Ruipu Energy entering the top 10 ranks.

China's top 20 power battery installed capacity in 2020

In 2020, the cumulative installed capacity of power lithium-ion batteries in my country will be 63.3GWh, an increase of 1.8% year-on-year. From the perspective of battery types, the installed capacity of ternary power batteries, lithium iron phosphate power batteries and other battery types are 39.7GWh, 23.2GWh and 0.4GWh respectively, accounting for 62.7%, 36.7% and 0.6% respectively.

Power battery cathode materials present 5 major development trends

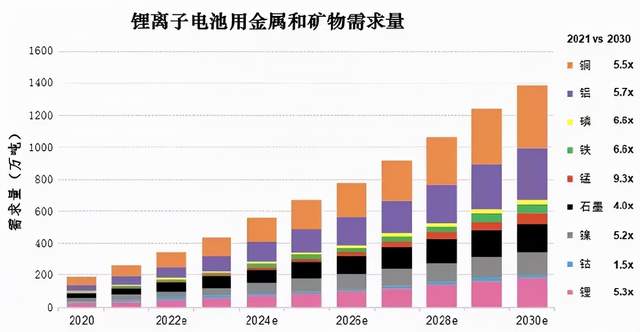

Hu Jian, senior vice president of Shanghai Nonferrous Network Information Technology Co., Ltd., said that global nickel resources are mainly distributed in Indonesia, the Philippines, Canada and other places. China is heavily dependent on imports from Indonesia/Philippines; global cobalt resources are mainly distributed in Congo, Australia, Cuba, etc. , China’s cobalt raw materials mainly rely on imports from Congo (DRC); global lithium resources are mainly distributed in Australia, Chile and other places, and domestic lithium raw materials rely on Western Australia imported concentrates.

Xu Aidong, Chief Engineer of Beijing Antai Technology Information Co., Ltd., Secretary-General of China Nonferrous Metals Industry Association Cobalt Industry Branch, and Executive Deputy Secretary-General of Nickel Industry Branch pointed out that although China lacks nickel, cobalt and lithium resources, it has the world’s largest battery material market and most The complete industrial chain is the main player of nickel, cobalt and lithium in the world. In 2020, the global output of nickel-cobalt-manganese ternary cathode materials was 438,000 tons, of which China's output was 208,000 tons, accounting for 47.5%. In 2020, China’s export volume of ternary cathode materials was 33,000 tons, a year-on-year increase of 73.93%, of which South Korea accounted for 43.51%, and Poland accounted for 34.33%. With the gradual production capacity of the Polish power battery plant, China’s exports to Poland in the future Ternary cathode materials will continue to increase.

Wei Qingmeng, chairman of Guangxi Manganhua New Energy Technology Development Co., Ltd., said that in the cost structure of power batteries, cathode materials account for about 50%.

Lithium ion cathode materials mainly include:

①Lithium iron phosphate, lithium iron manganese phosphate;

② Nickel cobalt manganese, nickel cobalt manganese aluminum, nickel cobalt aluminum;

③Lithium cobaltate, lithium nickelate;

④Layered lithium manganate, spinel aluminum nickel manganate;

⑤Manganese-based materials such as lithium manganate and manganese-rich lithium.

The main sodium ion cathode materials include:

①Copper, iron and manganese materials;

②Prussian white material based on ferromanganese;

③Manganese-based Prussian white material;

④Manganese-based high-manganese Prussian white and other materials.

The current development trend of cathode material technology is:

High nickel (three-element increase nickel content); high-manganese (a mixed ternary lithium manganate, lithium-rich manganese base); high voltage (three-element increase charging voltage, nickel-manganese binary); decobaltization (lithium iron phosphate , Cobalt-free nickel-manganese binary); delithiation (sodium ion battery).

In the future, the demand for manganese-based battery materials will continue to grow. After 2030, it is estimated that the demand will reach more than 1 million tons per year. In addition, the mixed application of elements such as lithium, sodium, manganese, iron and nickel will continue to grow.

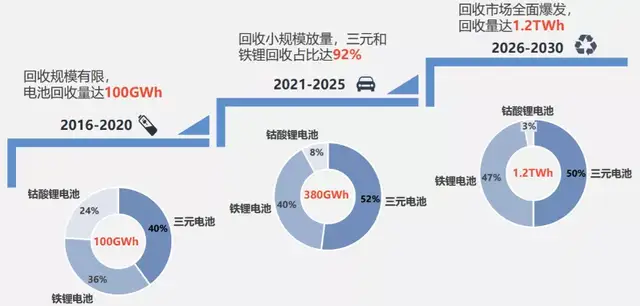

Hu Jian pointed out that in the next five years, power battery cathode materials will continue to be ternary + lithium iron phosphate; the demand for metals in the new energy industry will continue to increase, and domestic power batteries will consume nickel, cobalt, and lithium. Increases by 42%, 23%, and 35% respectively, the consumption of copper by domestic power batteries and charging piles will increase by 38%. In addition, new energy is about to enter the blue ocean of battery recycling, and it will fully explode after 2025, and the amount of used batteries will reach 1.2 TWh.

The five ASEAN auto industries have more potential for development

Xu Haidong said that in recent years, the ASEAN region has witnessed rapid economic growth and the automobile industry has great development and investment value. In the future, with the implementation of RCEP, it will further stimulate economic growth in Southeast Asia, increase GDP, trade and per capita income in the ASEAN region, and in the long run will promote the demand for auto consumption in the region and provide room for growth in the auto market. In addition, ASEAN countries are rich in resources and should become a key area for China's foreign investment. It is recommended that Chinese auto companies make full use of development opportunities such as RCEP and the “One Belt, One Road” initiative, combined with local industrial policies and investment environment, to actively deploy the Southeast Asian market and promote development in the region. However, given that the development level of ASEAN countries is quite different, and the market and consumption characteristics are not the same, enterprises should fully evaluate, adapt to local conditions, and have their own priorities in investment layout.

From the perspective of the three major indicators of total economic volume (mainly GDP), population size (resident population), and economic growth momentum (economic growth rate), among the ten ASEAN countries, the auto market is relatively large (considering exports) and the auto industry has relatively development potential. The main countries (considering investment) are Thailand, Indonesia, Malaysia, the Philippines and Vietnam.

At present, self-owned brand auto companies such as SAIC, Geely, and Great Wall are accelerating investment in the ASEAN region. China's SUVs and pickups are still relatively competitive in the ASEAN market where the infrastructure is not yet complete. Moreover, China's new energy vehicle technology already has export advantages, Thailand, Malaysia and other countries focus on energy conservation and carbon reduction, and new energy vehicle companies investing in ASEAN also have certain technological and industrialization advantages.

Liu Yanlong suggested that Chinese enterprises should seize opportunities such as the “Belt and Road” construction and international production capacity cooperation, establish international R&D institutions, actively carry out overseas layouts, and promote industrial cooperation to shift to high-end links in the industrial chain such as cooperative research and development and brand cultivation. The association will cooperate with professional institutions to actively assist Chinese companies to accelerate the construction of manufacturing bases overseas and accelerate their integration into the global market.

Xu Aidong pointed out that in 2021, in order to encourage the import of domestic resource products that are in demand, my country will reduce the temporary import tax rate of non-alloy nickel products (75021090, 75040010) to 1%. Sumitomo nickel that is not imported from Japan may have zero tariffs, which will help reduce the import cost of nickel products in my country. With a large number of Chinese companies investing in nickel hydrometallurgy projects in Indonesia, a large amount of nickel and cobalt intermediate products are expected to be shipped back to China from 2022 to supplement the shortage of power battery raw materials.